Can Sole Traders Get an LEI in the UK?

A simple answer comes first: yes, a sole trader in the UK can get a Legal Entity Identifier, or LEI.

That point matters because many people still assume LEIs are only for limited companies, LLPs, large funds, or banks. In practice, the LEI framework is wider than that. If a sole trader is acting in a business capacity and a broker, bank, custodian, or reporting obligation requires an LEI, one can be issued.

Can a UK sole trader obtain an LEI?

The key reason is found in the LEI data model itself. GLEIF, the organisation that oversees the global LEI system, includes SOLE_PROPRIETOR as an entity category. That category is defined as an individual acting in a business capacity.

So, while a sole trader is not a separate legal person in the same way as a limited company, the LEI system still recognises that business form for identification purposes. This is the point that clears up most confusion.

An LEI is a unique 20-character alphanumeric code linked to reference data about the entity. Each LEI is unique to one entity only, and the related record is public through the Global LEI Index. That public record is based on verified reference data collected by the issuing organisation.

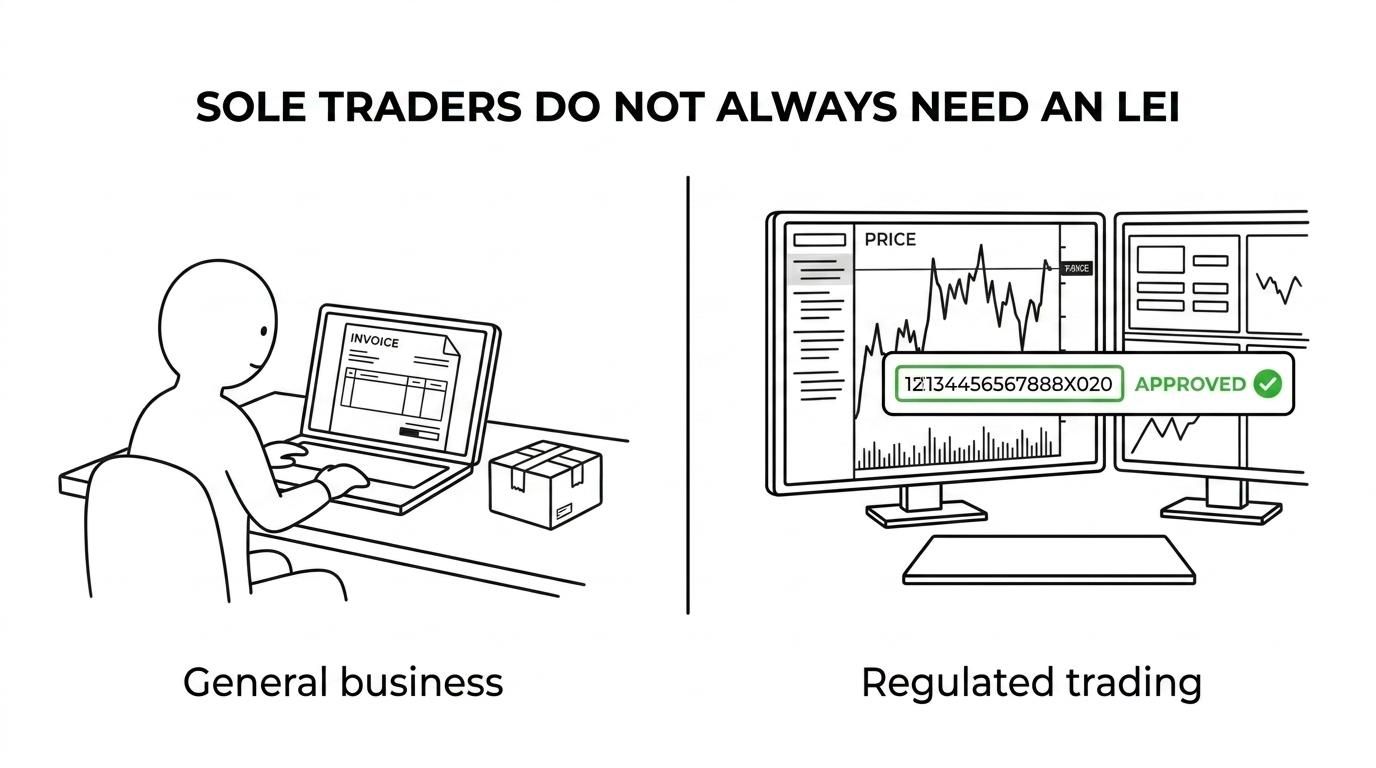

Why sole traders do not always need an LEI in the UK

Eligibility and necessity are not the same thing.

A UK sole trader may be able to obtain an LEI, but that does not mean every sole trader must have one. Many do not need one in day-to-day trading, invoicing, or general business activity. The requirement usually appears when regulated financial activity is involved, or when a financial institution asks for one before allowing a transaction to proceed.

This is why the question is often asked at the moment a trade is about to be placed, rather than when the business first starts operating.

A useful way to look at it is this:

- selling ordinary goods or services

- opening some business relationships

- dealing in certain financial instruments

- working through a broker or investment platform

- meeting transaction-reporting requirements

When an LEI matters for UK sole traders

For many sole traders, the practical issue is not theoretical eligibility. It is whether a counterparty insists on an LEI before processing a transaction.

The FCA has made this especially relevant under UK MiFIR. Its guidance states that firms subject to UK MiFIR transaction reporting obligations cannot execute a trade on behalf of a client who is eligible for an LEI and does not have one. That means the absence of an LEI can stop a transaction from happening.

In plain terms, a sole trader may start hearing about LEIs in situations like these:

- Broker account use: a platform may request an LEI before permitting trades in reportable instruments

- Bank or custodian onboarding: the institution may need the code for its own compliance process

- Professional investment activity: certain transactions may trigger reporting expectations

- Cross-border dealing: overseas counterparties may ask for a globally recognised identifier

- Entity transparency checks: the LEI can support standardised identification in regulated settings

This is why an LEI can move from “probably not needed” to “needed quite urgently” with very little notice.

UK MiFIR and sole trader LEI requirements

UK MiFIR is one of the clearest regulatory drivers behind LEI demand. The FCA guidance is aimed at firms with transaction reporting obligations, and it explains that those firms cannot execute a trade for an eligible client without an LEI.

The phrase “eligible client” matters. Not every client in every circumstance falls into that category. Still, where a sole trader is treated as eligible for an LEI in relation to the transaction, the firm placing the trade may not be able to proceed until the identifier is active.

That can create avoidable delay. A trader may have funding in place, an account ready, and an investment decision made, yet still be blocked because the identification requirement has not been sorted out beforehand.

For sole traders who deal with financial instruments, it is sensible to ask the broker or bank a direct question early on: Will you require an LEI for this activity? That saves time and gives clarity before any deadline becomes pressing.

What an LEI record for a sole trader contains

An LEI is not just a number. It sits alongside a public record with core reference data, often called Level 1 data. GLEIF explains that this includes identifying information such as the official name of the entity and its registered address.

For a sole trader, the record is tied to the business identity recognised for LEI purposes, using verified reference data from appropriate local or official sources. The exact supporting information can vary depending on the issuer and the nature of the sole trader’s registration details.

The public nature of the LEI system is one of its strengths. It gives market participants a consistent way to identify who is involved in a transaction.

| Question | Short answer for UK sole traders |

|---|---|

| Can a sole trader get an LEI? | Yes, if the business is eligible and the required data can be verified |

| Is an LEI always mandatory? | No, not for all sole traders |

| When does it become important? | When a broker, bank, or reporting rule requires it |

| Is the LEI record public? | Yes |

| Does it last forever without maintenance? | No, it must be renewed annually |

How a UK sole trader applies for an LEI

The application process is usually straightforward, especially when handled through an LEI issuer or registration agent that works regularly with UK entities. GLEIF notes that legal entities seeking an LEI must provide accurate reference data to the issuing organisation. In some cases, the issuer can pull data from a local registration authority, which reduces the amount of manual input needed.

For sole traders, the exact form of evidence can depend on how the business is registered and what official reference points exist. The aim is always the same: to verify that the applicant is the entity it claims to be.

Common parts of the process include:

- Business identity details: the trading name or official business name used for the LEI record

- Address information: registered or principal business address details

- Local registration data: any relevant official number or registry reference

- Authorised applicant details: confirmation that the person applying is entitled to do so

- supporting documents where needed

A helpful provider can make a real difference here, especially if a sole trader is applying for the first time and wants to avoid back-and-forth over missing data.

How long LEI issuance can take for a sole trader

Timing depends on the application quality, the ease of verification, and the service level chosen. Where the source data is easy to validate, issuance can be very fast. Where extra checks are needed, it can take longer.

For a sole trader trying to meet a trading deadline, speed matters. That is why many applicants prefer a UK-focused registration route with clear support by phone or email, particularly if a broker has already requested the LEI.

The most efficient approach is to apply before the transaction is imminent.

LEI renewal rules for UK sole traders

An LEI is not a one-off administrative step that can be forgotten. The FCA states that an LEI must be renewed annually by providing updated information to the Local Operating Unit, which may charge an annual fee.

This annual renewal keeps the record current and maintains the LEI’s active status. If a sole trader’s address or other reference data changes, those details should be kept accurate. Current data is part of what gives the LEI system its value.

That means a sole trader should keep an eye on:

- renewal date

- current business address

- official registration data

- whether the LEI status remains active

Multi-year renewal options can be useful for applicants who want less admin, especially if the LEI will be needed for ongoing market activity rather than a one-off transaction.

Choosing the right LEI route in the UK

Not all application routes feel the same from the user’s side, even though the end product is the same global identifier. Some applicants want the lowest possible cost. Others care more about support, speed, or help with unusual entity types.

For UK sole traders, the most practical choice is often a provider that handles UK entities regularly and offers a clear path for registration, renewal, or transfer. Support matters when the entity type is less familiar to the applicant than a standard limited company setup.

When comparing options, it helps to look for:

- Transparent pricing: no confusion over first-year and renewal costs

- Fast turnaround: useful when a bank or broker has set a deadline

- UK support access: phone and email help in clear English

- Data maintenance: updates to reference data when details change

- Renewal flexibility: annual, multi-year, or transfer-and-renew choices

A sole trader who expects repeated use of the LEI should also check how easy renewal will be a year later, not just how quick the first issuance appears today.

Practical checks before a sole trader applies for an LEI

Before submitting an application, it helps to confirm exactly why the LEI is needed and how the institution involved describes the requirement. Sometimes a broker’s compliance team will specify the entity name format they expect, or whether the LEI should be active before account approval, before trading, or before settlement.

That small check can prevent rework.

It is also sensible to make sure the business details used in the application match the official records the issuer is likely to verify. Consistency speeds things up and reduces the chance of manual review.

If a sole trader has been told an LEI is required, there is no need to assume the request is mistaken simply because the business is not incorporated. The LEI framework does accommodate sole proprietors, and UK financial firms may need that identifier before they can proceed with certain regulated transactions.