Do I Need an LEI for a Business Bank Account?

Opening a business bank account in the UK does not usually mean you need an LEI straight away. For most standard current accounts, banks focus on identity checks, company documents, beneficial ownership details, and anti money laundering checks rather than a Legal Entity Identifier.

The picture changes when that account is linked to regulated financial activity. If the bank account is used to access investment services, hold certain securities, or place reportable trades through a bank or investment firm, an LEI can move from optional to necessary very quickly.

What an LEI means for a business bank account in the UK

An LEI is a 20 character code used to identify legal entities in financial transactions. It is part of the Global LEI System and links to public reference data about the entity, including its legal name, address, and in many cases ownership information. GLEIF describes it as a global identifier for legal entities participating in financial transactions.

That is the key point. An LEI is not a general business account number, and it is not a universal requirement for opening every business bank account. It is mainly tied to regulated financial activity.

In the UK, the FCA states that firms subject to UK MiFIR transaction reporting obligations cannot execute a trade for an eligible client that does not have an LEI. So if your bank account is simply there to receive income, pay suppliers, run payroll, or hold cash, an LEI will often not be mandatory. If the same business then starts trading financial instruments through a regulated firm, the position can change.

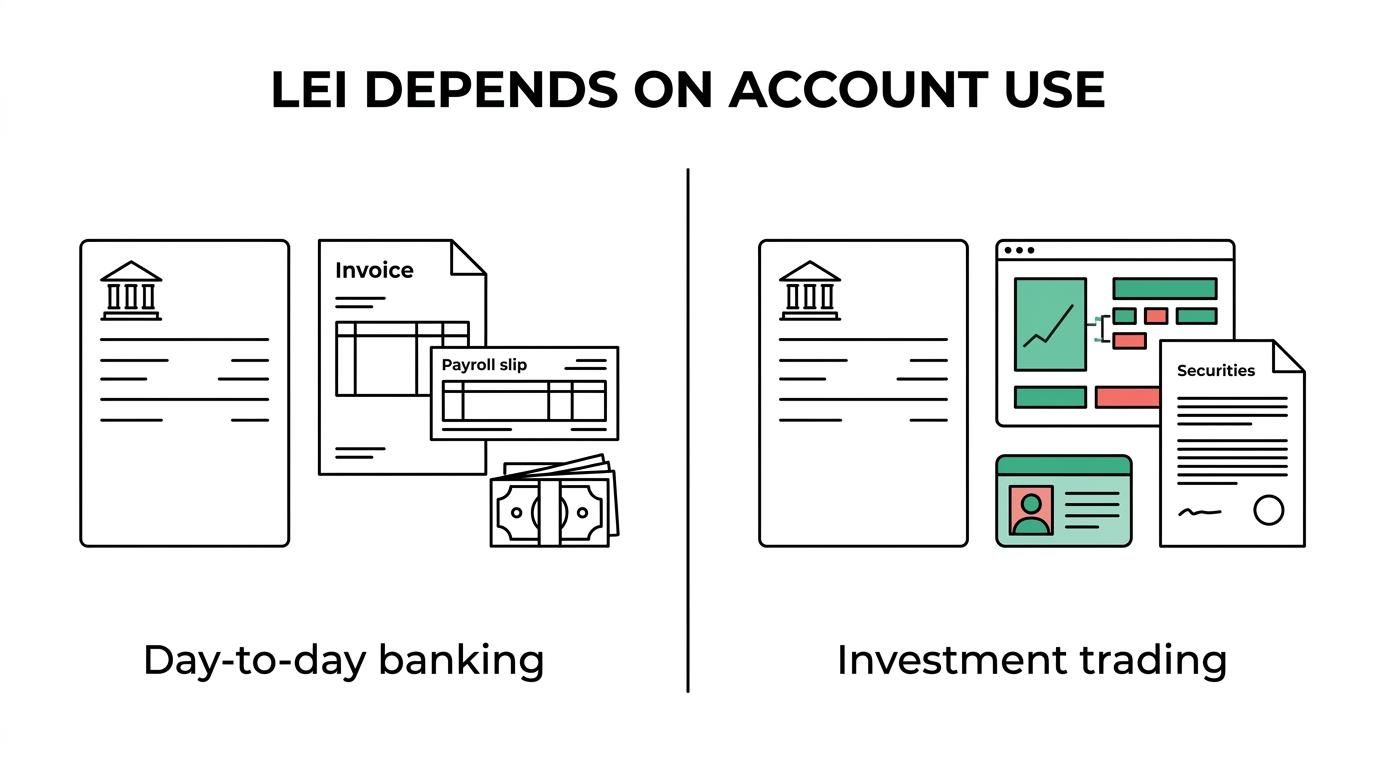

A simple way to think about it is this:

- Standard day to day banking

- Payments and cash management

- Savings or deposit facilities

- Investment and securities trading

- Regulated transactions that trigger reporting

The first three commonly do not require an LEI by default. The last two often do, depending on the entity and the service being used.

What official sources say about LEI requirements

Official guidance is fairly consistent once the distinction is clear.

The FCA frames the LEI as mandatory where a regulated firm needs it in order to meet transaction reporting rules. Its position is practical and direct: if a reportable trade cannot be reported without an LEI, the firm cannot execute the trade for an eligible client.

GLEIF takes the wider global view. It explains that any legal entity entering into a financial transaction is eligible for an LEI, while the legal duty to have one comes from national regulators and market rules. That means eligibility is broad, but obligation depends on the activity and the jurisdiction.

The Bank of England adds another useful layer. It points to the practical value of LEIs in linking data sets, improving analysis, and supporting better risk assessment. So even where an LEI is not legally required to open an account, some financial institutions may still see it as useful in onboarding, data quality, and entity verification.

| Official source | What it says | What it means for a bank account |

|---|---|---|

| FCA | A firm subject to UK MiFIR reporting cannot execute certain trades for an eligible client without an LEI | LEI can become mandatory if the account is used for reportable investment activity |

| GLEIF | Any legal entity entering a financial transaction is eligible for an LEI; legal requirements come from regulators | LEI is not a blanket banking requirement, but it is relevant across financial markets |

| Bank of England | LEIs help connect data and improve risk assessment | A bank may value an LEI for onboarding and data clarity, even outside strict trade reporting |

Business bank account situations where an LEI may be requested

If you are opening a straightforward business current account, there is no clear official rule saying every UK business must have an LEI first. A bank may ask for one in specific cases, but that is different from a universal opening requirement.

Where businesses often run into LEI requirements is when the bank account is connected to investment or treasury activity. A company opening an account to hold cash from operations is in a different category from a company opening an account for bond purchases, listed securities, derivatives, or other reportable instruments.

This is also relevant for entities beyond limited companies. The FCA notes that LEIs identify legal entities and structures including companies, charities, and trusts. Pension arrangements and other legal structures may also need one where they interact with regulated financial markets.

Common examples include:

- Usually not required: a normal business current account for trading income, bills, salaries, and tax payments

- Sometimes requested: a business account that is part of a wider banking relationship involving treasury products or investment services

- Often required: execution of reportable trades through a bank, broker, or investment firm covered by UK MiFIR rules

- Worth checking early: charity, Trusts, or pension banking arrangements that include investments or custody services

That last point matters because many organisations assume LEIs are only for large corporates. Official sources do not limit them in that way. The need is driven by the type of financial activity, not by a company’s size or profile.

Why banks and investment firms ask for an LEI

From a bank’s perspective, an LEI creates a reliable link between the customer and a standardised set of legal entity reference data. That improves consistency when names differ slightly across systems, when group structures are layered, or when cross border financial activity is involved.

For regulated firms, the issue is even sharper. Transaction reporting obligations depend on accurate entity identification. A missing LEI can stop a transaction before it starts. That is why businesses often first hear about LEIs not from Companies House or HMRC, but from a bank, broker, custodian, or investment platform.

There is also a broader operational benefit. An LEI can support cleaner onboarding, reduce repeated entity identification questions, and make it easier to keep reference data aligned. The Bank of England has highlighted the wider value of LEIs in improving data linkages and supporting financial stability objectives.

This is why a bank might say, in effect, “You do not need an LEI to hold the account, but you do need one to use this investment feature.”

Which UK entities can obtain an LEI

If your organisation is a legal entity or legal structure, there is a good chance it is eligible. GLEIF’s position is broad: any legal entity that enters into a financial transaction can obtain an LEI.

In UK practice, that can include a wide range of organisations that use banking and investment services:

- Limited companies

- LLPs

- Charities

- Trusts

- Pension schemes

- Funds

- Certain public sector bodies

- Other recognised legal structures

An LEI is issued under the global standard ISO 17442 and appears in the Global LEI Index. Registration is handled through authorised channels connected to the Global LEI System, often involving accredited issuers sometimes referred to as Local Operating Units.

How to decide whether you should apply for an LEI now

If your only aim is to open a plain business bank account, you may not need to act yet. It is sensible to ask the bank one direct question before applying: “Is an LEI required for this account, or only for specific products and trading services?”

That single question can save time. It separates everyday banking from regulated market activity, which is where most LEI requirements arise.

A practical checklist helps:

- Account purpose: Is this account only for payments and cash management, or will it support investments and securities activity?

- Regulated services: Will a bank, broker, or investment firm execute trades for the entity?

- Entity type: Is the account being opened for a company, charity, trust, pension, or another legal structure that may be eligible for an LEI?

- Bank policy: Has the institution made the LEI part of its onboarding or product access rules?

- Future plans: Could the business move into treasury investments, hedging, or market transactions within the next year?

If the answer points towards trading or regulated investments, getting the LEI in place early is often the smoother option. It avoids last minute delays when a transaction is ready to go and the reporting requirement appears.

How LEI timing affects account opening and trading access

Timing matters more than many businesses expect. A bank may open the account without an LEI, then pause access to a related investment product until one is active and valid. That can be frustrating if the business assumed bank onboarding and trading readiness were the same thing.

LEIs also need renewal to remain current. An expired LEI can create fresh issues with firms that rely on up to date entity data. For organisations that trade regularly, renewal is part of routine compliance rather than a one off task.

This is one reason many entities prefer a provider that offers simple applications, renewal reminders, and support in plain English. Speed can matter too, especially when a trade, settlement, or mandate is waiting on the identifier.

Getting an LEI quickly if your bank or broker requests one

When an LEI is needed, the process is usually straightforward if your legal details are ready. You will normally need the entity’s registered name, registration information, address details, and supporting records that match official registers.

Many UK entities choose an official registration agent because the process is faster and support is easier to access. A service focused on UK applicants can be useful where the entity is a trust, charity, pension, or another structure that needs a little more care during application.

What tends to matter most is:

- Speed: urgent issuance options can help when a bank or investment firm is waiting

- Support: phone and email help can make unusual entity types much easier to process

- Renewals: keeping the LEI active avoids problems later

- Data updates: free updates to reference data can save administrative effort

For businesses that expect to use investment services, obtain regulated market access, or face onboarding questions from a bank, arranging the LEI before it becomes urgent can keep the banking relationship moving without interruption.