LEI for estates and executors: when a will, estate or executor may need an LEI

Most executors in the UK will never need a Legal Entity Identifier. Probate, by itself, does not create a general LEI requirement, and a person does not need an LEI simply because they have become an executor.

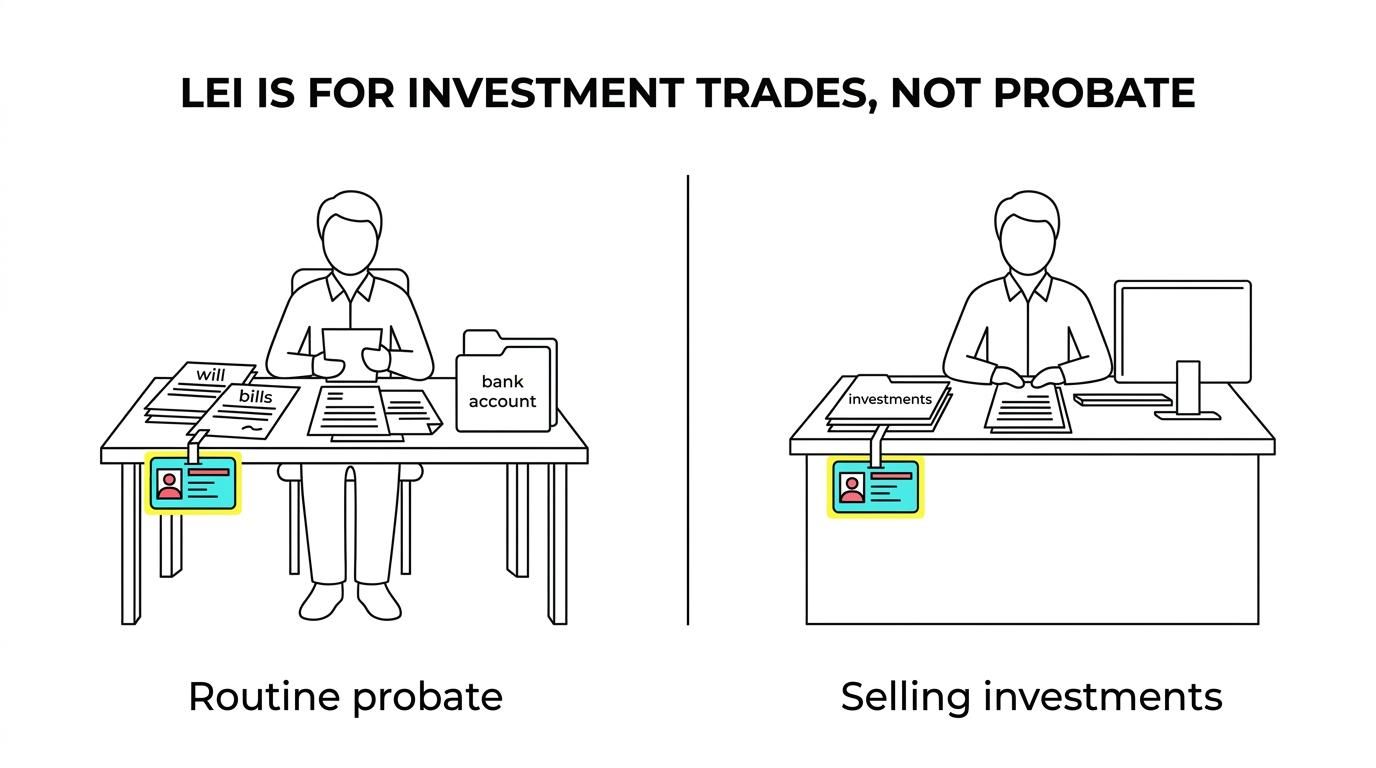

The point at which LEIs enter the picture is much narrower and much more practical: when estate assets include investments that need to be sold, transferred, or managed through a firm that is subject to UK financial reporting rules.

That distinction matters, because it can save executors time at a stage when estates are already full of paperwork, deadlines, and sensitive decisions.

The basic UK rule on LEIs for estates and executors

In the UK, an LEI is mainly a financial markets identifier. It is used where a legal entity or eligible structure is involved in transactions in certain financial instruments, and the investment firm handling that transaction must report it under UK MiFIR.

This is the source of the familiar rule often shortened to “no LEI, no trade”. If the relevant client is a legal entity or structure that is eligible for an LEI, the investment firm may need that LEI before it can execute the transaction.

For executors, that means the real question is not whether the estate exists, or whether probate has been granted. The real question is whether the estate, or a related structure such as a trust, is being treated as the client in a reportable investment transaction.

Most estates do not need an LEI at all.

Why a will does not have its own LEI

A will is not a legal entity. It is a legal document setting out wishes, appointments, and instructions, but it is not itself the kind of body that would usually receive an LEI.

The same applies to an executor in a personal capacity. Someone does not obtain an LEI merely because they are acting as executor or personal representative. The LEI question usually attaches to the entity or structure involved in the transaction, not to the office-holder as an individual.

That is why estate cases can feel confusing at first. People often ask whether “the will needs an LEI” or whether “the executor needs an LEI”, when the more accurate question is whether the estate arrangement being used to hold or deal with investments needs one.

Estate transactions that commonly trigger an LEI requirement

The main trigger is investment activity, not routine administration. If executors are collecting cash balances, paying funeral expenses, settling debts, dealing with tax, or distributing money to beneficiaries, there is no general UK rule saying an LEI is needed just for those steps.

The position can change when the estate holds financial instruments and a broker, bank, custodian, or investment firm needs to process a transaction that falls within reporting rules.

Typical examples include:

- Quoted shares

- Corporate bonds

- Units in funds and ETFs

- Derivatives and structured products

Where those assets sit inside an estate, a trust, or a comparable structure, the firm involved may ask for an LEI before it can act. This is especially common where the account is not being treated as a simple personal holding.

Common UK estate activities and whether an LEI is likely

The easiest way to think about it is to separate ordinary probate tasks from market transactions.

| Estate activity | LEI likely needed? | Comment |

|---|---|---|

| Opening or operating a standard estate bank account | Usually no | No general probate rule requires an LEI for this alone |

| Collecting cash, paying debts, tax, or funeral costs | Usually no | These are ordinary administration steps |

| Selling listed shares through a broker | Often yes | The broker may need an LEI for a reportable transaction |

| Selling bonds or fund holdings | Often yes | These are commonly within financial reporting rules |

| Holding estate assets in a trust structure that trades investments | Often yes | Trusts are frequently treated as eligible structures |

| Transferring property or land | Usually no | This is not normally an LEI-triggering investment transaction |

| Dealing with overseas custodians or foreign securities | Sometimes to often | Cross-border firms may require an LEI as part of their process |

This table does not replace case-specific advice, though it does reflect the pattern executors most often see in practice. Ordinary probate work usually does not need an LEI. Investment transactions are where the requirement tends to appear.

Why cross-border estate assets often create LEI questions

When an estate includes overseas shares, international funds, foreign custody accounts, or assets already held through a non-UK platform, the chance of an LEI request goes up.

That is partly because the LEI is a global identifier. It gives intermediaries a standard way to identify the entity or structure involved, even where several jurisdictions, account providers, and reporting systems are in play.

It is also why executors are sometimes asked for an LEI even when they had not expected it from a probate point of view. The request may not be coming from succession law at all. It may be coming from the broker’s compliance team, the custodian’s onboarding rules, or the way a foreign market participant classifies the account.

A cross-border estate is still an estate, but the operational demands around it are often more exacting.

Practical LEI checks for executors before selling investments

Before selling shares or other marketable assets, executors are wise to clarify how the broker or investment firm is classifying the client. That single point can decide whether an LEI is needed immediately, later in the process, or not at all.

A few simple checks can prevent delays at the point of sale.

- Check the client name: ask whether the transaction will be booked in the name of the estate, a trust, or the individual personal representatives.

- Confirm the asset type: ask whether the holding is a financial instrument covered by transaction reporting rules.

- Gather authority papers: have probate documents, trust papers, or other evidence of authority ready in case the firm requests them.

- Ask about timing: if a sale is urgent, check whether the trade will be blocked until the LEI is issued.

- Check renewal status: if the estate or related structure already has an LEI, make sure it is active and not lapsed.

These questions are simple, but they are often the difference between a clean transaction and a last-minute scramble.

Applying for an LEI for an estate-related structure in the UK

The application route depends on what exactly needs the LEI. If the relevant party is a company, the process is usually straightforward because registry information can be checked quickly. If the relevant party is a trust or another non-corporate structure linked to estate administration, the application may involve more manual review.

Executors should expect the registration agent or issuing framework to verify the identity of the entity or structure and, where needed, the authority of the people acting on its behalf. The exact documents can vary, especially in estate and trust cases.

In practice, applicants are often asked for some combination of the entity name, official registry data where available, ownership or control details, and supporting paperwork that shows who is authorised to act.

That variation is normal.

How an LEI helps executors in practice

An LEI does not give executors their legal authority. Probate documents, the will, and the rules governing personal representatives do that work.

What the LEI does is remove an identification barrier in financial markets. It gives brokers, custodians, and reporting systems a standard reference point for the estate-related structure they are dealing with.

That can help in several ways:

- Faster broker onboarding

- Clearer transaction reporting

- Less ambiguity in cross-border holdings

- Easier identification across multiple intermediaries

For an executor trying to sell a portfolio efficiently, that can make a real difference. Not because the LEI changes the law of probate, but because it helps the financial system recognise the right party quickly and accurately.

When speed matters for an estate LEI application

Estate administration is not always slow and orderly. Sometimes assets need to be sold to settle liabilities, meet tax deadlines, or prepare a distribution that should not be held up by avoidable compliance issues.

In those situations, speed matters. A registration service that can process applications quickly, provide support in plain English, and help with renewals or transfers can save valuable time. LEI Service acts as an official registration agent of Ubisecure RapidLEI and focuses on UK entities, including structures that may need an LEI for market transactions.

Where no extra checks are needed, issuance may be available very quickly, ranging from minutes to 48 hours, with a faster option for urgent applications submitted before the stated cut-off time. Support by phone and email can also be useful where an executor, solicitor, or administrator needs help working out what should be registered and how.

The right preparation often matters as much as the speed of the service itself.

Key signs an executor should ask about an LEI

Executors do not need to become market regulation specialists, but they should pause and ask the LEI question when certain signs appear.

- A broker says a trade cannot proceed yet

- The estate includes listed securities or funds

- Assets are held through a trust

- A foreign custodian asks for entity identification

- A sale is time-sensitive and compliance checks have started

If any of those apply, it is sensible to raise the issue early with the firm handling the assets.

An LEI is not a universal probate formality in the UK. It is a targeted requirement that appears when estate administration meets regulated investment activity. For many executors, that point never arrives. For others, especially those handling portfolios, trusts, or international holdings, getting the LEI in place early can keep an estate moving when timing matters most.