LEI in the UK: a plain-English guide to the Legal Entity Identifier system

If you trade, report derivatives, or deal with regulated financial counterparties in the UK, an LEI is often less of a nice-to-have and more of a gatekeeper. Many organisations first hear about it when a broker, bank, fund platform, or compliance team says a transaction cannot proceed without one.

That can make the subject sound more obscure than it really is. In plain terms, a Legal Entity Identifier is a globally recognised identity code for organisations. Once the jargon is stripped away, the system is fairly logical, and the UK uses the same international framework as everyone else.

What a Legal Entity Identifier means in the UK

A Legal Entity Identifier, usually shortened to LEI, is a 20-character alphanumeric code that identifies a legally distinct entity involved in financial transactions. It is based on the international standard ISO 17442 and sits within a global public data system rather than a UK-only register.

That last point is useful to keep in mind. A UK company, charity, trust, pension arrangement, fund, or other eligible entity does not get a special British version of an LEI. It receives a code from the same worldwide system used across markets and jurisdictions.

The LEI system was created to make counterparties easier to identify and to reduce confusion caused by similar names, group structures, and inconsistent local identifiers. It supports two broad data layers: who the entity is, and where available, who owns whom.

| Part of the LEI system | What it does |

|---|---|

| Regulatory Oversight Committee | Public sector oversight of the framework |

| GLEIF | Oversees operational integrity and global LEI data availability |

| LEI issuer | Validates data, issues the LEI, publishes records |

| Registration agent | Helps entities apply, renew, transfer, and maintain LEIs through an issuer |

In the UK, this matters because the LEI is woven into financial regulation. It is not just an admin code sitting quietly in a database. In the right context, it determines whether trading and reporting can happen at all.

Why UK organisations need an LEI

The strongest UK use cases sit within transaction reporting and derivatives reporting. Under UK MiFIR, firms that must submit transaction reports cannot execute trades for an eligible legal-entity client if that client does not have an LEI. Under UK EMIR, UK counterparties entering into derivative trades need an LEI for reporting.

That means the LEI often becomes urgent only when a firm tries to trade, report, or complete onboarding. A company may have operated happily without one for years, then suddenly find it needs an LEI within a tight deadline because a broker or reporting obligation has brought it into scope.

A few common triggers include the following:

- Equity or bond trading

- Derivatives reporting

- Broker onboarding

- Fund and treasury activity

- Counterparty due diligence

- Regulatory reporting

The practical benefit is straightforward. A standard public identifier makes it easier for firms, regulators, and market infrastructures to recognise the same entity consistently across systems.

Which UK entities may need an LEI

Many people assume LEIs are only for banks and listed groups. They are not. A wide range of UK legal entities may need one, depending on the activity involved and the requirements of the institution they deal with.

This can include private limited companies, public companies, charities, trusts, pension vehicles, funds, special purpose entities, and other organisations with a recognised legal or reporting identity. Some arrangements outside ordinary Companies House records can still qualify, though they may require more manual checks.

A simple way to think about it is this: if an organisation is entering a regulated financial relationship, there is a fair chance someone in the chain will ask for an LEI.

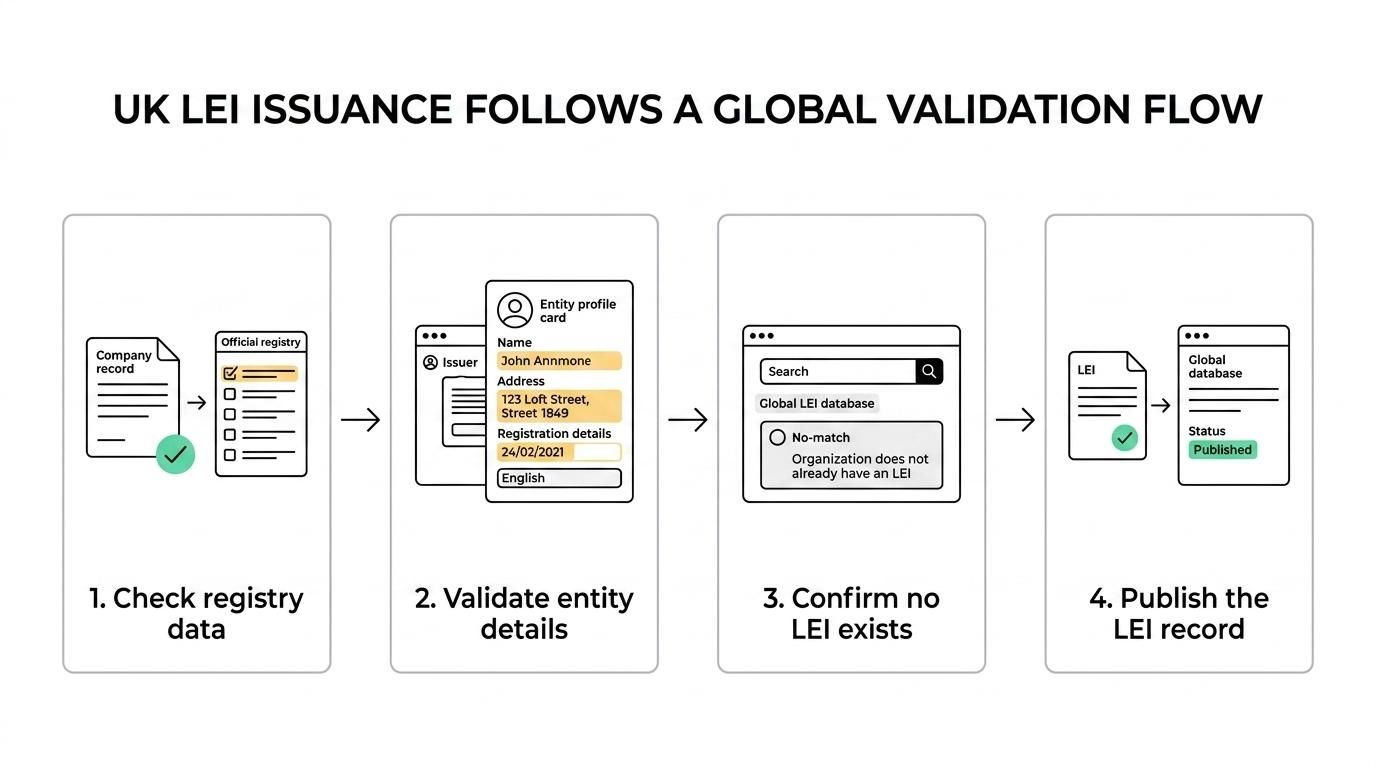

How LEI application and issuance work in the UK

A UK entity can apply directly through a GLEIF-accredited LEI issuer, or it can use a registration agent that handles the process with the issuer on its behalf. The LEI itself is issued within the global LEI framework, not by the FCA.

That distinction matters. The FCA uses LEIs within the rules it supervises, but it does not act as the issuing body. In other words, the UK regulatory need and the global issuance process sit side by side.

In practical terms, the application flow is usually quite simple. Basic registry data is checked first, then the entity’s details are validated, and the issuer confirms that the organisation does not already have an LEI. Once approved, the LEI record is published into the global system.

For many standard UK entities, this is faster than people expect, especially where registry information is clear and the ownership picture is straightforward.

What information is needed for a UK LEI application

The starting point is usually the entity’s legal name or registration number. For a standard UK company, much of the core data can often be matched against Companies House records. For trusts, pensions, funds, and other less standard structures, more manual input may be needed.

The issuer or registration agent also needs to know that the person applying is authorised to act for the entity. If parent relationship data is required, the application may ask for direct and ultimate parent details, or for a valid reporting exception where that information cannot be supplied.

Typical application inputs include:

- Entity details: legal name, registration number, registered address, country of formation

- Applicant details: name, email address, phone number, authority to act for the entity

- Registry checks: confirmation of official record data where available

- Ownership details: parent information or an accepted exception reason

- Contact information: details needed in case validation questions arise

Accuracy matters here. An LEI application is not difficult, but it does rely on clean source data. If the official record is out of date, the application can slow down.

LEI renewal in the UK and why annual checks matter

An LEI is not a one-off registration that can be forgotten. It must be renewed each year so the reference data can be revalidated and kept current.

That annual cycle is a core feature of the system rather than an irritating add-on. The value of an LEI comes from current data. If the legal name, address, registry status, or parent relationship information changes, those updates need to be reflected properly.

For firms trading or reporting under UK rules, a lapsed LEI can create real friction. Even if the code itself still exists in the database, an out-of-date status may block a transaction or trigger extra compliance questions.

Multi-year renewal options can make planning easier, and automatic renewal can reduce the risk of an LEI slipping past its expiry date. That is especially useful for organisations with several entities or lean internal teams.

Using a registration agent for UK LEI applications

Many entities prefer not to deal with issuer processes directly. That is where a registration agent can be useful. A registration agent sits between the applicant and the issuing organisation, helping with data entry, checks, renewals, transfers, and support.

LEI Service operates in this category as an official LEI registration agent of Ubisecure RapidLEI. For UK applicants, that means access to a simplified application process, English-speaking phone and email support, and help with new registrations, renewals, and transfers through an accredited issuing structure.

For straightforward UK cases, speed can be a genuine advantage. LEI Service states that issuance can take from about 10 minutes to 48 hours in standard cases, with VIP delivery in around 2 hours for orders placed before 5pm. More complex cases can take longer, which is normal where additional validation is needed.

Pricing and service structure are also part of the decision. At the time of writing, the service offers low-cost options for single-year and multi-year terms, free updates to LEI reference data, assisted applications, and bulk ordering for organisations managing more than one entity.

When a transfer or renewal service makes sense

An LEI does not have to stay with the same service provider forever. If an entity already has an LEI and wants simpler support, different pricing, or easier renewal management, a transfer and renewal service can be the sensible route.

This is often relevant where the original LEI was obtained in a rush, perhaps through a trading platform or overseas provider, and the entity now wants a more direct support channel. The LEI remains the same identifier. What changes is the administration and renewal pathway.

That can be particularly helpful for UK entities that want:

- lower renewal costs

- one contact point

- phone support

- bulk management

- clearer renewal reminders

Practical checks before you apply for an LEI in the UK

A little preparation makes the process faster. Before starting, it helps to confirm the exact legal name of the entity, registry details, the authority of the applicant, and whether parent data will be required.

If the LEI is needed for a live trade or deadline-sensitive reporting event, timing should be checked early rather than late. Waiting until the dealing desk is ready to execute is rarely the cheapest or calmest option.

A sensible pre-application checklist looks like this:

- Confirm the legal entity that needs the LEI, not just the group name.

- Check whether the entity already has an LEI in the public database.

- Gather registry and contact details before starting the form.

- Decide whether a direct issuer route or a supported registration agent route suits you better.

- Put the renewal date into your compliance calendar as soon as the LEI is issued.

For many UK organisations, the LEI is best seen as core market infrastructure. It supports access, reporting, identification, and trust in a single code. When the process is handled cleanly, it becomes one of those compliance tasks that quietly does its job and stays out of the way.