LEI vs BIC vs ISIN: What's the Difference?

LEI, BIC and ISIN are often mentioned together because they appear in the same trading, reporting and settlement workflows. The important point is simple: they identify different things, so choosing the wrong one creates avoidable breaks in compliance, operations and data matching.

TL;DR: Summary

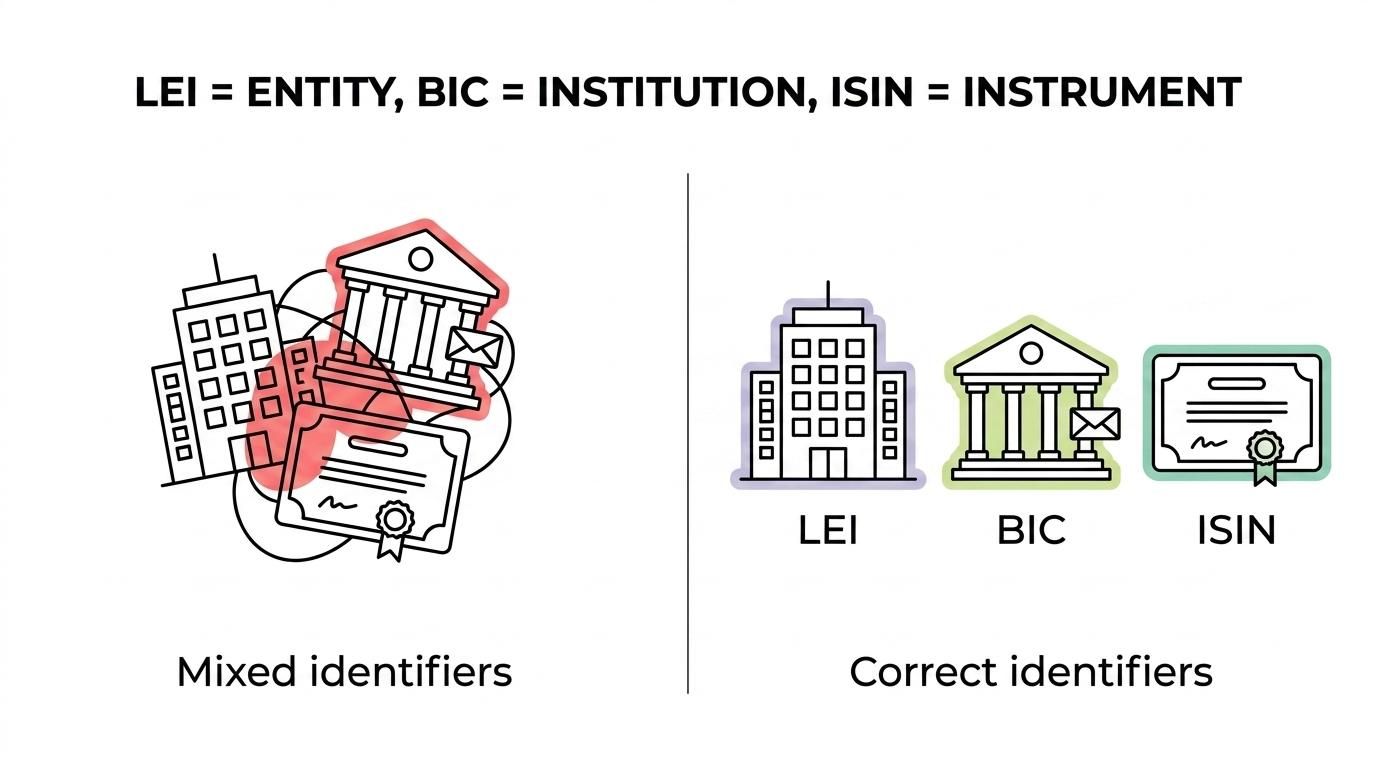

- LEI, BIC and ISIN are not substitutes: an LEI identifies a legal entity, a BIC identifies a business party or institution for messaging and routing, and an ISIN identifies a financial instrument.

- The standards are different and easy to separate: LEI is a 20-character code under ISO 17442, BIC is an 8-character code under ISO 9362, and ISIN is a 12-character code under ISO 6166.

- Use an LEI when the question is “which legal entity is this?”; use a BIC when the question is “which institution or messaging party is involved?”; use an ISIN when the question is “which exact security or instrument is being traded or referenced?”

- GLEIF publishes LEI-to-BIC and LEI-to-ISIN mapping relationships, so the identifiers can be linked across market systems even though they sit at different identification layers.

- In practical UK workflows, one transaction can require all three: the ISIN for the bond or share, the LEI for the issuer or counterparty, and the BIC for settlement or financial messaging.

That distinction matters because many teams still ask whether one code can replace another. It cannot. A cleaner way to think about the issue is to start with the object being identified: entity, institution or instrument.

What is the core difference between LEI, BIC and ISIN?

LEI, BIC and ISIN identify different objects. GLEIF defines the LEI as a 20-character ISO 17442 code for legal entities, SWIFT manages the 8-character BIC under ISO 9362, and ISO 6166 assigns the 12-character ISIN to securities.

An LEI answers the question, “Which legal entity is this?” That could be a company, fund, charity, pension vehicle or trust acting as a reportable legal counterparty. Each LEI is unique to one entity and connects to verified reference data in the Global LEI Index, including core identity information and ownership-related data where available.

A BIC answers a different question: “Which business party or institution is involved in this message or transaction flow?” In practice, BICs are deeply tied to financial messaging and routing. A common mistake is to assume the BIC always identifies the customer. In many cases, it identifies the bank or institution handling the message instead.

An ISIN answers, “Which exact instrument is this?” If a company has multiple share classes or a bond programme with many issues, the ISIN distinguishes one instrument from another. That is why an issuer can have one LEI but many ISINs.

How do LEI, BIC and ISIN compare at a glance?

The quickest comparison is object, standard and code length. GLEIF’s LEI is 20 characters, SWIFT’s BIC is 8, and the ISO 6166 ISIN is 12.

After the labels, the operational difference becomes clearer when you look at where each code is used in real systems.

- LEI: Legal entity identification for reporting, onboarding and counterparty transparency

- BIC: Business party identification for financial messaging, routing and institutional processing

- ISIN: Security or instrument identification for trading, reference data and portfolio records

- Main question: Who is the entity, who is the institution, or what is the instrument?

- Typical risk if misused: Failed reporting matches, payment or settlement breaks, or wrong-instrument booking

If two codes appear to overlap, they usually do so only because the same event touches several layers at once. A bond trade can involve an issuer, a security and a settlement institution, which is exactly why multiple identifiers appear together.

What LEI registration options can UK entities use?

Only the LEI usually requires active registration by the entity or its agent. LEI Service , accredited Local Operating Units and selected institutional workflows can all be used, while BICs and ISINs follow different issuance models.

For many UK organisations, the practical question is not whether to “get a BIC or ISIN” personally, but how to obtain and maintain the LEI that counterparties, venues or reporting obligations require. BICs are issued within the SWIFT ecosystem, and ISINs are assigned to instruments within securities issuance and market data frameworks.

“LEI Service issues LEIs from 10 minutes to 48 hours, with a VIP 2-hour option for orders placed before 5pm.”

That means the choice is usually about service model, internal workload and support quality rather than the identifier’s meaning.

- LEI Service: UK-focused registration agent of Ubisecure RapidLEI offering registration, renewal, transfer, free reference-data updates, and phone and email support.

- Direct with an accredited issuer or LOU: Suitable for teams that prefer to manage applications and renewals internally.

- Through a bank, broker or intermediary workflow: Useful when LEI handling is bundled into a wider onboarding process.

- Via enterprise data or corporate services providers: More common for groups managing large portfolios, funds or bulk renewals.

A sensible trade-off applies here. If the entity needs fast turnaround or support for edge cases, an assisted route can save time. If the compliance team already manages identifier operations at scale, a direct route may be enough.

When do you need an LEI rather than a BIC or ISIN?

Choose an LEI when the subject is the legal entity itself. GLEIF’s LEI is the right code when a UK company or trust must be identified as a counterparty, issuer or reportable organisation.

Step 1 is to ask what is being identified in the workflow. If the form, trade report or venue rule is asking for the legal person or organisation, start with the LEI. That covers situations where a company, charity, pension entity or fund needs to be named consistently across systems.

Step 2 is to check whether the requirement is entity-based or transaction-based. If the obligation refers to the reporting entity, issuer entity, fund manager entity or counterparty entity, the LEI is usually central. Pro tip: if the question contains the words “legal entity”, “issuer”, “counterparty” or “reporting party”, the LEI is often the first identifier to verify.

Step 3 is to confirm status and reference data. An inactive or expired LEI can still create operational friction even when the number itself is correct. If the legal name, registered address or corporate structure has changed, the LEI record should reflect that.

When is a BIC the correct identifier?

Use a BIC when the workflow is about institution-level messaging or routing. SWIFT’s BIC is the right code when the system needs to know which business party should receive, send or process a transaction message.

Step 1 is to look for a network or settlement instruction context. If the process involves financial messaging, payments, routing or institutional addressing, a BIC is likely relevant. Think of the BIC as operational plumbing for institutions rather than as the universal identity of every client in the chain.

Step 2 is to separate the institution from the underlying customer. This is where teams often go wrong. A bank’s BIC may identify the bank handling the message, while the client behind the trade still needs its own LEI. If the regulator wants the entity behind the activity, a BIC alone will not solve that need.

Step 3 is to map the BIC back to the entity layer where needed. GLEIF’s BIC-to-LEI relationship work is useful here because it helps link institutional messaging identifiers to legal entity identity data. That improves matching across reference data, compliance and post-trade systems.

When is an ISIN the correct identifier?

Use an ISIN when the workflow is about the instrument being traded or referenced. ISO 6166 makes the ISIN the standard code for unique identification of securities and referential instruments.

Step 1 is to ask whether you are identifying a share, bond, ETF, note or other security. If yes, you need the instrument identifier, not the entity identifier. An issuer can have one LEI and hundreds of instruments, so the LEI cannot tell you which exact security is in scope.

Step 2 is to check the precision required. Portfolio accounting, settlement instructions, market data feeds and execution records usually need instrument-level precision. A common misconception is that the issuer name is enough. It is not enough when different issues have different maturities, terms, currencies or share classes.

Step 3 is to connect the instrument back to the issuer where relevant. ISIN records can sit within a wider data ecosystem that includes issuer legal entity information, which is where LEI becomes valuable. If you need both “what was traded?” and “who issued it?”, ISIN and LEI work together.

How are LEI, BIC and ISIN linked in market data?

They are separate identifiers but they are operationally linked. GLEIF publishes BIC-to-LEI relationship data and has worked with ANNA on ISIN-to-LEI relationship files so systems can connect entity, institution and instrument layers.

This matters because real workflows rarely stay inside one data model. Compliance reporting may start with a legal entity, execution systems may carry an instrument code, and settlement messages may use institutional routing identifiers. Without mapping, teams end up reconciling the same event in three different languages.

“LEI Service notes that LEI mapping files include BIC and ISIN mappings, helping firms connect entity data with trading and reporting records.”

GLEIF announced a BIC-to-LEI relationship file in February 2018. GLEIF and ANNA also piloted daily open-source ISIN-to-LEI relationship files in April 2019. Those milestones matter because they show the market has been moving towards cross-identifier consistency for years, not towards a single universal replacement code.

Can one transaction include LEI, BIC and ISIN together?

Yes, one transaction can legitimately contain all three. A bond trade can carry an ISIN for the instrument, an LEI for the legal entities involved, and a BIC for the institutions handling settlement or messaging.

Take a simple case. A UK asset manager buys a bond through a bank. The bond itself is identified by ISIN. The legal entities, including the asset manager and often the issuer or reporting parties, are identified with LEIs. The institution sending or receiving settlement messages may be identified with a BIC.

If the workflow is front-office trading, the ISIN often appears first. If it moves into compliance reporting, the LEI becomes critical. If it moves into payment, messaging or settlement rails, the BIC becomes relevant. Seeing all three in one lifecycle is normal, not redundant.

What mistakes cause identifier mismatches in reporting and settlement?

Most mismatches come from identifying the wrong layer. The usual failures are using a BIC where an LEI is required, using an issuer name where an ISIN is required, or letting LEI reference data go stale.

One recurring error is to treat the executing bank’s BIC as if it identifies the investing entity. It may identify the bank perfectly while saying nothing precise about the client behind the trade. Another is to assume an issuer’s LEI is enough to identify a bond. It is not enough if the issuer has multiple debt issues.

Data freshness is the next risk. A legal name change, merger, address change or lapsed renewal can break matching even when everyone “knows” which entity is meant. Pro tip: if the transaction fails validation but the code looks correct, check the status and reference data before you rebook anything.

How should UK firms keep LEI reference data accurate?

Keep the LEI current at source and review it whenever legal details change. The Global LEI Index is the authoritative directory for LEI reference data, so accuracy there supports cleaner reporting and counterparty matching elsewhere.

A practical routine works well. First, confirm that the registered legal name matches official records. Second, review registered address and entity status after any corporate event. Third, renew on time so the LEI remains active in the periods when venues, banks or reporting systems need it.

“LEI Service provides free updates to LEI reference data, which is useful when an entity’s legal details change between registration cycles.”

This is one area where service support can matter. UK entities that rarely deal with identifier maintenance often need help with transfers, renewals or ownership-related questions, while larger groups may prefer a bulk or multi-year process to reduce admin effort. The key point stays the same: the LEI is most useful when the reference data behind it stays current.