LEI vs Company Registration Number vs VAT: what’s the difference?

Many UK organisations end up dealing with more than one official identifier at the same time. A company might have a Companies House number from incorporation, a VAT number from HMRC, and an LEI because it trades in regulated financial markets. The problem is that these numbers can look equally formal while serving completely different purposes.

That is where confusion starts.

A finance team may be asked for “the company number”, “the VAT number”, or “the LEI” in different settings, sometimes on the same day. Using the wrong one can slow a transaction, create a reporting problem, or leave an application incomplete.

Why LEI, company registration number and VAT number are often mixed up

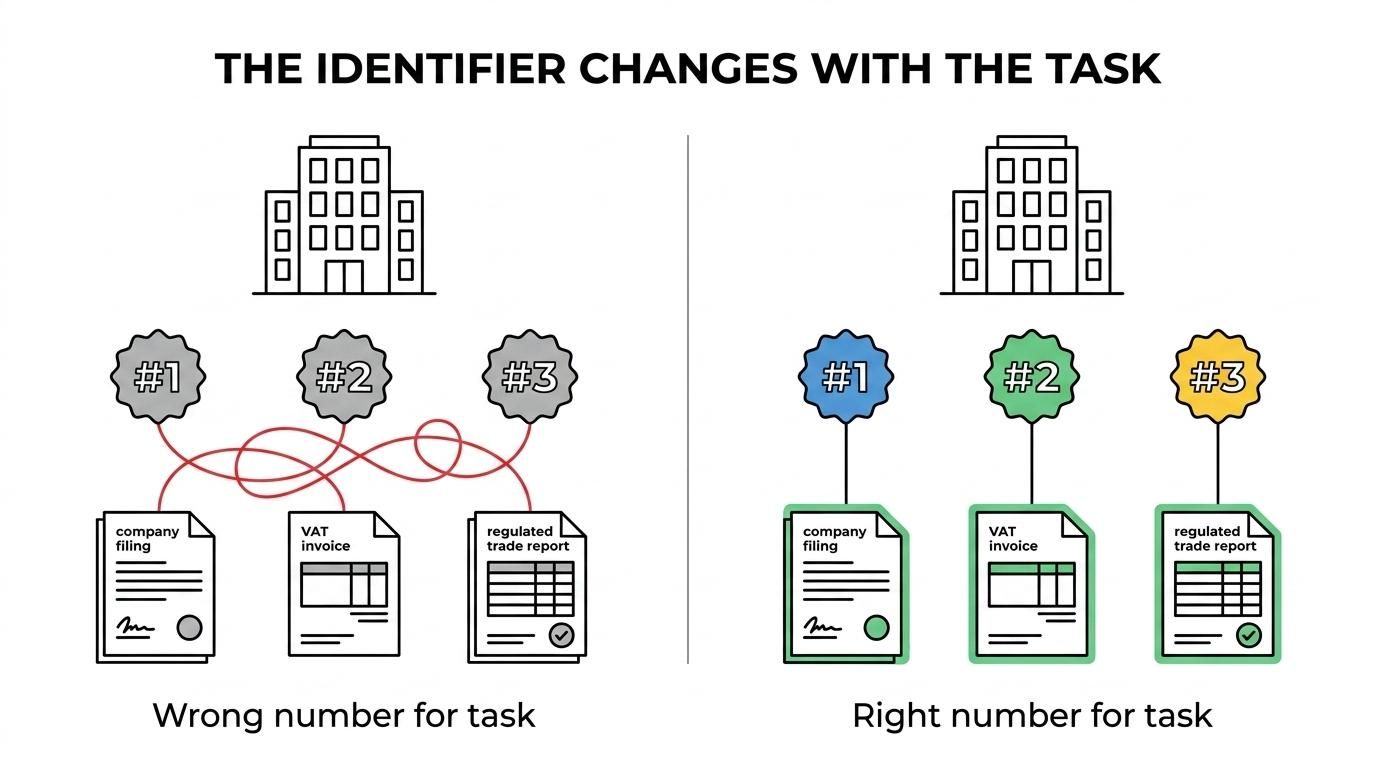

These identifiers all help identify an organisation, but they do not identify it in the same legal or regulatory system. One sits in company law, one sits in tax administration, and one sits in global financial market reporting.

The overlap in everyday business activity makes the distinction less obvious. A limited company filing accounts uses its Company Registration Number, registering for VAT uses its company details and often its Company Registration Number, and entering regulated trades may require an LEI. The same organisation is involved, but the identifier changes with the task.

A few simple patterns explain most of the confusion:

- Official numbers attached to one organisation

- Requested by banks, brokers, accountants and regulators

- Often stored together in onboarding files

- Easy to confuse when forms use generic wording

What an LEI number is and what it is used for

An LEI, or Legal Entity Identifier, is a global identifier for legal entities involved in financial transactions. It is a 20 character alphanumeric code based on the ISO 17442 standard and is designed to answer a practical question: who exactly is the organisation behind this transaction?

Unlike a UK company number, an LEI is not limited to incorporated companies. It can apply to companies, funds, pension schemes, charities, trusts and other legal entities, depending on eligibility and market activity. Its core purpose is transparency in financial markets.

The LEI system is overseen globally by the Global Legal Entity Identifier Foundation, with codes issued through accredited issuing organisations. In UK practice, the LEI becomes especially relevant when an entity falls within transaction reporting or derivatives reporting rules. The Financial Conduct Authority has made clear that firms subject to UK MiFIR and UK EMIR rules need the correct identification of counterparties, and in many cases that means an LEI.

This is why an LEI matters even to businesses that do not think of themselves as “financial institutions”. A corporate entering certain derivatives for hedging, a pension arrangement involved in regulated activity, or an investment vehicle transacting through a broker may all need one.

What a Company Registration Number is in the UK

A Company Registration Number, usually shortened to CRN, is the official number assigned when a company is incorporated at Companies House. It is the organisation’s statutory identity within the UK company register.

For most companies in England and Wales, the CRN is an eight digit number. Scottish and Northern Irish entities may have prefixes such as SC or NI. Once assigned, it stays with the entity for its life on the register.

A CRN is not optional for an incorporated company. If the business is a limited company or LLP registered in the UK, it has one. It appears on the certificate of incorporation, Companies House filings, and often on websites, invoices, order forms and other official communications.

The scope here is purely different from an LEI. A CRN proves the existence of a company in the UK corporate register. It does not replace an LEI in regulated market reporting, and it does not replace a VAT number for tax administration.

What a VAT number is and when HMRC issues it

A VAT number is a tax identifier issued by HMRC when a business registers for Value Added Tax. In the UK, this is typically a nine digit number and is often shown with the GB prefix in cross-border or formal invoicing contexts.

The key point is that not every business has a VAT number. A business only gets one when it registers for VAT, either because it must or because it chooses to do so voluntarily. HMRC currently requires VAT registration once taxable turnover passes the relevant threshold, which is £90,000 at present.

That means a small incorporated company can have a CRN but no VAT number. A sole trader can have a VAT number but no CRN. A charity might have an LEI for market activity yet have no VAT registration, depending on what it does and how its supplies are treated.

VAT numbers are practical tools for tax compliance. They are used on VAT invoices, VAT returns, and systems where input tax and output tax are recorded. Without a VAT number, a business cannot issue a proper VAT invoice or reclaim VAT in the normal way.

One easy way to think about it is this:

- LEI: global market identity for legal entities in financial transactions

- CRN: UK incorporation identity at Companies House

- VAT number: UK tax identity for VAT registration and reporting

Quick comparison of LEI, CRN and VAT number

The differences become clearer when the three are viewed side by side.

| Identifier | Issued by | Typical format | Who usually has one | Main purpose |

|---|---|---|---|---|

| LEI | Global LEI System through accredited issuers | 20 character alphanumeric code | Legal entities involved in regulated financial activity or needing market identification | Financial transaction reporting and counterparty identification |

| Company Registration Number | Companies House | Usually 8 digits, sometimes prefixes like SC or NI | UK incorporated companies and LLPs | Statutory company identification |

| VAT number | HMRC | Usually 9 digits, often used with GB prefix | VAT registered businesses | VAT invoicing, filing and tax compliance |

The practical takeaway is straightforward. These numbers do not compete with each other. They sit in different systems and can all be valid for the same organisation at the same time.

When an LEI is required instead of a company number or VAT number

A common mistake is to assume that a CRN should be enough because it already identifies the company. In regulated financial markets, that is not how the rules work. The LEI exists precisely because a domestic company number is not suitable as a global market identifier.

If a UK entity enters into derivative transactions subject to UK EMIR reporting, an LEI is generally required. If an investment firm must report transactions under UK MiFIR, it cannot simply substitute the client’s Companies House number. The entity needs the identifier accepted within that reporting framework, which is the LEI.

This matters for more than large banks. It can apply to:

- investment firms

- issuers and listed entities

- pension and investment structures

- corporates using derivatives for hedging

In these settings, the question is not “does the organisation exist?” The CRN already answers that for a company. The real question is “what is the globally recognised identifier for this legal entity in financial reporting?” That is where the LEI fits.

When a Company Registration Number is the correct identifier

A CRN is the right number when the issue is company law, legal existence on the UK register, or statutory filings with Companies House. It is the number used to file accounts, submit confirmation statements, record company changes, and verify an incorporated entity in official UK records.

It is also routinely requested by banks, suppliers, platforms and professional advisers when they want to confirm that a business is genuinely incorporated. In day to day administration, the CRN often does a lot of work behind the scenes.

Typical CRN uses include:

- Companies House filings: accounts, confirmation statements, officer changes

- Corporate documents: websites, letters, invoices and formal notices

- Due diligence checks: confirming incorporation and legal status

- Government processes: registrations or applications linked to the company register

A business that is not incorporated will not have a CRN, even if it has a VAT number. That distinction is especially important for sole traders and unincorporated partnerships.

When a VAT number is the correct identifier

A VAT number becomes the correct identifier when the issue is tax, taxable supplies, VAT invoices or VAT reporting to HMRC. If the activity involves charging VAT, reclaiming VAT, or filing VAT returns, the VAT number is the one that matters.

This number is tied to VAT registration status, not to incorporation status. That is why a sole trader can have one, and why some companies do not. It depends on VAT registration, not on the existence of a limited company.

In practical terms, the VAT number is usually needed when a business is:

- issuing VAT invoices

- submitting VAT returns to HMRC

- reclaiming input VAT on eligible costs

- showing VAT registration details in trade documentation

Northern Ireland rules can add another layer in goods trade with the EU, where the XI prefix may apply in the relevant circumstances. That is one more reason not to treat all business identifiers as interchangeable.

Common misconceptions about LEI, CRN and VAT numbers

One of the most persistent myths is that the LEI is only for banks. It is strongly associated with financial institutions, but the requirement reaches beyond them. Any legal entity caught by certain reporting rules or market participation requirements may need one.

Another misconception is that a VAT number proves incorporation. It does not. HMRC issues VAT numbers to different business types, including sole traders. A VAT number tells you about tax registration, not corporate status.

A third misconception is that the CRN can be used everywhere because it is the “main” number for a company. In UK company law, yes. In tax and financial market reporting, no.

How UK organisations can work out which identifier they need

The fastest way to separate these numbers is to ask what the task is actually for. Is it a company law filing, a VAT obligation, or a financial market reporting requirement? Once that is clear, the correct identifier is usually obvious.

A simple internal check can prevent a great deal of avoidable back and forth across finance, legal and compliance teams.

Ask these questions before submitting any form or trade request:

- Is this about incorporation or Companies House records? Use the CRN.

- Is this about VAT invoices, returns or HMRC VAT registration? Use the VAT number.

- Is this about regulated trading, counterparty reporting or market identification? Use the LEI.

For organisations active in several regulated or cross-border settings, it is wise to keep all three numbers recorded in one verified compliance file, with clear labels and renewal dates where relevant.

Getting an LEI quickly when a transaction depends on it

The LEI is the only one of these three identifiers that needs ongoing renewal to remain active. That often catches organisations by surprise. A company keeps its CRN for life, and a VAT number remains tied to VAT registration status, but an LEI must be renewed annually to stay active in the global LEI database.

That makes provider choice important. A specialist service can help reduce delay, especially where a trade or reporting deadline is close. LEI Service, an official registration agent of Ubisecure RapidLEI, supports UK entities with LEI registration, renewal and transfer, including assisted applications, multi-year renewal options, free updates to LEI reference data, and English-speaking phone and email support. For businesses that need a fast result, express and VIP turnaround options can be valuable.

The main point is simple: if your organisation is being asked for an LEI, a CRN or a VAT number, it is being asked for three different things. Knowing which system each number belongs to turns a confusing admin request into a clear compliance decision.