When do you need an LEI to trade? MiFIR, EMIR and UK reporting explained

For many UK organisations, the question is not whether an LEI is useful. It is whether a trade can happen without one.

That distinction matters because an LEI is often tied directly to market access and reporting. If a trade falls within UK MiFIR transaction reporting or UK EMIR derivatives reporting, a legal entity will usually need its LEI in place before the firm can execute the order properly or submit the required report. That can affect companies, charities, trusts, pension arrangements and other non-individual structures that participate in financial markets.

An LEI, or Legal Entity Identifier, is a unique 20-character alphanumeric code assigned to a legal entity through the global LEI system. It exists to make market participants identifiable across reporting regimes, venues and jurisdictions. In practical terms, it helps regulators and firms see who is trading, who is a counterparty to a derivative, and whether reporting data is consistent.

What a Legal Entity Identifier means for UK trading

The LEI is not a UK-only concept. It is issued through a global framework and can be obtained via accredited issuing organisations, often called Local Operating Units, or through official registration agents that work with them. That global structure matters because UK MiFIR and UK EMIR both rely on the same identifier format used across wider international reporting.

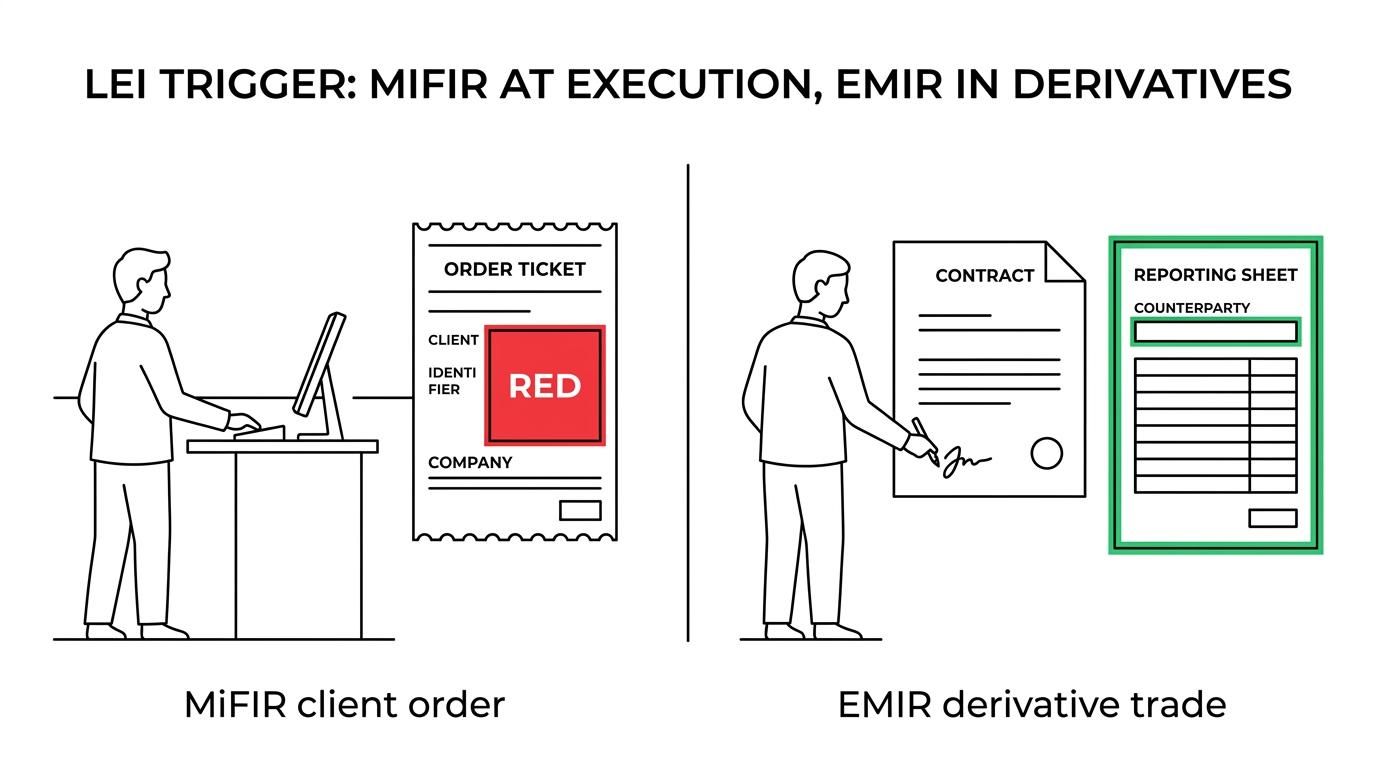

In market reporting, the LEI is the standard code used to identify legal entities. Under MiFIR rules, investment firms use it in transaction reports to identify clients that are legal persons. Under EMIR rules, LEIs are used to identify counterparties that are legal entities in derivative reporting. So while the regulations differ, the function of the LEI is remarkably consistent: it is the identity key that makes the reporting record usable.

This is also why the LEI is not just an administrative detail. If the reporting obligation exists, the missing LEI becomes a trading problem very quickly.

When UK MiFIR makes an LEI necessary before a trade

The clearest UK rule for pre-trade need comes from the FCA’s guidance on UK MiFIR transaction reporting. Firms subject to UK MiFIR reporting obligations will not be able to execute a trade on behalf of a client who is eligible for an LEI and does not have one. That is a firm, direct barrier to execution.

The same FCA material states that clients which are legal entities or structures, including companies, charities and trusts, need to arrange an LEI if they want a firm to act on their instructions or make a decision to trade on their behalf. In other words, if a UK investment firm is going to execute reportable transactions for a non-individual client, the LEI often needs to exist first.

That does not mean every financial activity by every organisation triggers MiFIR. The key point is whether the firm is subject to UK MiFIR transaction reporting for the transaction in question. Where it is, the LEI becomes part of the reporting infrastructure and can no longer be treated as optional.

Entities commonly affected include:

- Companies

- Charities

- Trusts

- Pension-related structures

- Other legal persons trading through an investment firm

A useful way to think about UK MiFIR is this: if the broker or investment firm has to file a transaction report that identifies the client as a legal person, the LEI is usually the required identifier. Without it, the firm may be unable to proceed.

When UK EMIR requires an LEI for derivatives reporting

UK EMIR addresses a different reporting stream. It focuses on derivatives, and the FCA has stated that all UK counterparties entering into derivative trades need an LEI in order to meet UK EMIR reporting obligations.

This is broader than a simple equities or bond dealing scenario. If an entity enters into a derivative contract, whether for hedging or another purpose, the reporting regime is likely to require the counterparty to be identified by LEI in the report submitted to a trade repository. The LEI is not just helpful here. It is part of the reporting dataset.

That means a UK company entering into an interest rate swap, a charity using a foreign exchange forward, or a trust involved in a derivative position may need the LEI before the trade is booked and reported. The reporting obligation sits behind the transaction, but it has very real front-end effects because firms, counterparties and reporting delegates need the identifier ready.

The practical impact of UK EMIR can be summed up like this:

- Derivative trade entered into: the UK counterparty will generally need an LEI for reporting

- Report sent to a trade repository: the legal entity is identified using its LEI

- No LEI available: reporting becomes defective or delayed, which creates compliance risk

UK MiFIR and UK EMIR compared at a glance

The two regimes are often mentioned together, yet they apply in different ways. One is centred on transaction reporting by investment firms. The other is centred on derivatives reporting by counterparties.

| Rule | What triggers the LEI need | Who is identified | Practical effect |

|---|---|---|---|

| UK MiFIR | A reportable transaction executed by a firm subject to transaction reporting | The client that is a legal person | A firm may be unable to execute the trade without the client’s LEI |

| UK EMIR | Entering into a derivative trade with a UK reporting obligation | The legal entity counterparty | The derivative report requires the counterparty LEI |

| EU MiFIR or EU EMIR | Relevant EU reporting obligations | Legal persons or counterparties | The same global LEI format is used across the reporting framework |

The comparison is useful because many organisations hear “LEI for trading” and assume there is a single rule. There is not. The need depends on the regulatory route the trade follows.

Which UK entities usually need an LEI for trading

The FCA’s wording is broad enough to catch more than standard trading companies. It refers to legal entities and structures, including companies, charities and trusts. That is significant in the UK, where investment activity is often carried out by a wide range of vehicles, not just corporates.

Take a few common examples. A limited company placing investment orders through a broker may need an LEI where UK MiFIR transaction reporting applies. A charity with a discretionary manager may need one if the manager is making investment decisions and reporting the resulting transactions. A trust or pension-related vehicle entering into a derivative for hedging may need one under UK EMIR.

A simple test helps:

- Is the client or counterparty a legal entity or legal structure rather than a private individual?

- Is the activity a reportable securities transaction under UK MiFIR or a derivative transaction under UK EMIR?

- Will a firm, broker, manager or reporting delegate need to identify that entity in a regulatory report?

If the answer to those questions is yes, the LEI requirement is usually close behind.

This is one reason many organisations apply for an LEI before they begin account opening or trading negotiations. Waiting until a trade is ready can introduce avoidable delays, especially where the order is time-sensitive or the entity has a more complex constitutional structure.

LEI renewal and active status for ongoing UK reporting

There is an important nuance here. The FCA has said that annual LEI renewal applies to firms subject to UK MiFIR transaction reporting obligations, but there is no requirement under Article 13(3) for firms to ensure that a client’s or counterparty’s LEI has been renewed.

That point is often misunderstood. It does not mean renewal is irrelevant. It means the legal duty described by the FCA is narrower than many assume. In practice, many market participants still prefer an active, renewed LEI because current reference data supports cleaner onboarding, easier counterparty checks and more reliable reporting records.

For organisations that trade regularly, renewal remains a sensible part of compliance housekeeping. A lapsed status can invite operational questions even where the rule itself does not create a direct block in every case.

Practical steps to obtain an LEI before trading

If an LEI is likely to be needed, speed matters. The entity should apply through the global LEI system, either directly with an accredited issuer or via an official registration agent. The core application usually requires basic legal entity reference data, and the details must match the official records for that entity.

For UK organisations, choosing a provider with clear support can make the process much easier, especially where the applicant is a trust, charity, pension structure or another entity that does not fit the standard company template. Fast issuance is often valuable when a broker, counterparty or reporting deadline is already in view.

A practical checklist helps keep things moving:

- Check the activity: is the planned transaction caught by UK MiFIR or UK EMIR reporting?

- Confirm the entity type: company, charity, trust, pension vehicle or another legal structure

- Apply early: do not wait until the trade date if execution depends on the LEI

- Match the records: entity name and registration details should be consistent with official source data

- Plan renewal: keep the LEI record current if trading or reporting will continue

There is a very simple commercial reality behind all of this. Firms cannot report properly without the right identifiers, and regulators expect the reports to be complete, accurate and on time. When the entity is a legal person and the trade falls into the relevant reporting regime, the LEI moves from a compliance formality to a precondition for action.

That is why the most effective approach is often the least dramatic one: check the rule, confirm the reporting path, and get the LEI arranged before the trade reaches the dealing desk.